Most Western analysis of Iran’s drone program centers on key facilities: HESA at Shahin Shahr, Shahed Aviation Industries at Badr Air Base, Qods Aviation Industries near Mehrabad, and a handful of IRGC sites. Operation Epic Fury targeted these on February 28, aiming to hit production capacity.

Strikes caused real damage: satellite imagery showed several damaged buildings at HESA’s Shahin Shahr complex, Iran’s main production site for Ababil and Shahed-series drones. Other strikes also hit Shahed-linked facilities in Isfahan, cratered the runway at the Ali Akbar Drone Base in Ahvaz, set IRIS Shahid Bagheri ablaze, and hit Parchin east of Tehran.

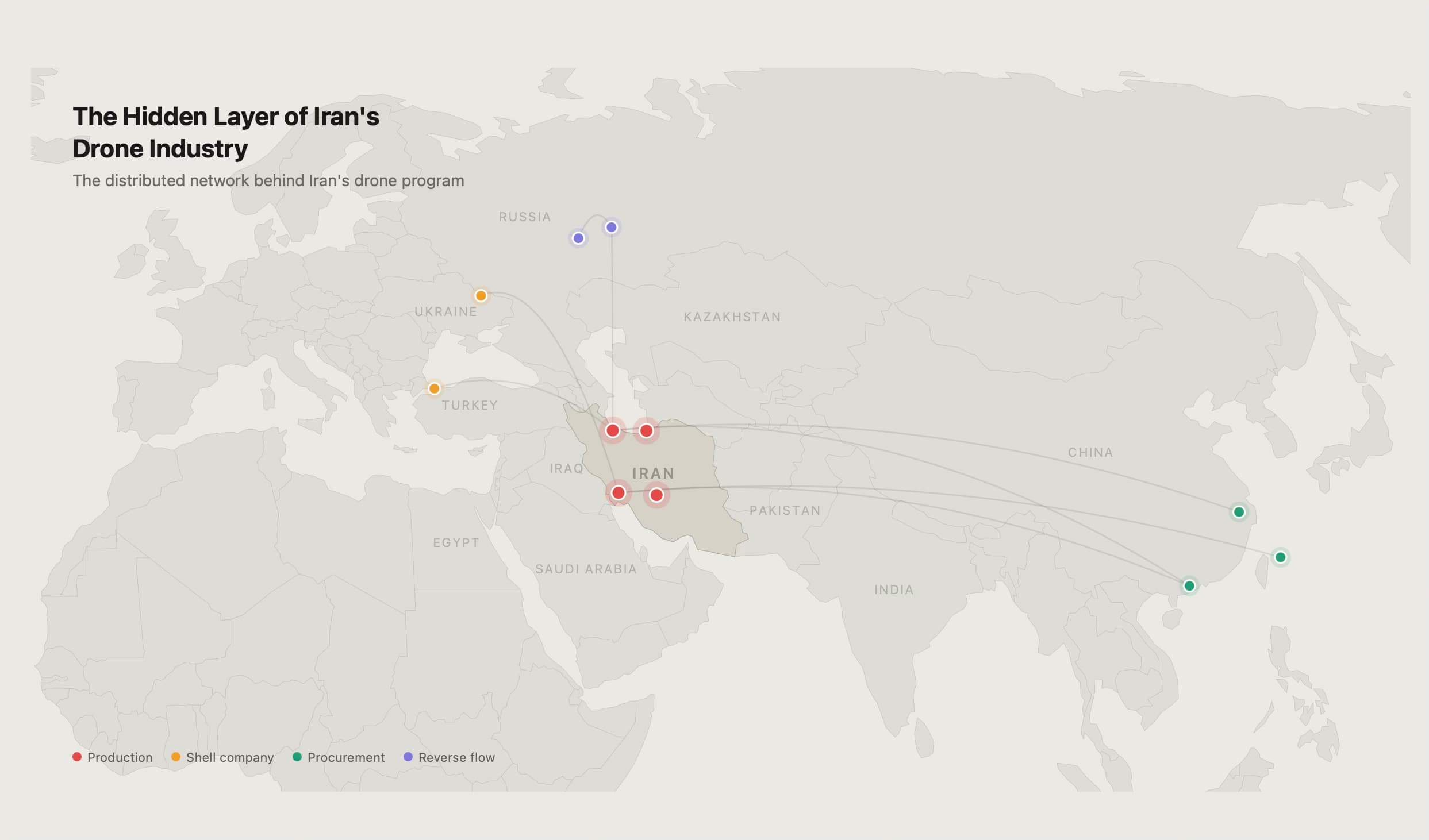

These losses matter, but they only damage the visible side of Iran’s drone industry, not the full system keeping it going.

Iran’s drone industry is more than a few factories. It is a layered ecosystem of state-owned manufacturers, IRGC-linked developers, private subcontractors, and foreign procurement networks. Destroying key facilities may disrupt output, but that does not collapse the entire ecosystem.

At the top sit the state firms under the Ministry of Defense and Armed Forces Logistics, along with their aviation subsidiaries. HESA and Qods Aviation Industries remain the best-known names. Alongside them, the IRGC runs its own development track through the Aerospace Force Self-Sufficiency Jihad Organization and affiliated research centers tied to the Shahed series.

The most important layer for reconstitution is the least visible one: the private sector.

In November 2023, Iran’s deputy defense minister said MODAFL worked with roughly 7,000 enterprises nationwide, about 40 percent of them “knowledge-based companies.” Not all of those firms are drone-related. But the figure matters because it points to the structure of the defense base itself: broad, distributed, and deeply intertwined with nominally civilian industry.

A centralized drone industry can be mapped and stopped, while a distributed one is harder to break.

Open-source work by the Wisconsin Project’s Iran Watch has shown that these firms support different segments of drone production rather than operate as a single vertically integrated system. That is what makes the network resilient.

The most important layer is the engines. Oje Parvaz Mado Nafar Company, better known as Mado, produces reverse-engineered engines used in the Shahed-131 and Shahed-136. Other firms sit around that engine ecosystem, servicing imported designs, absorbing tacit engineering knowledge, and building the technical base for indigenous reproduction. This is one of the few genuine choke points in the system. Final assembly can be dispersed. Precision engine production cannot.

Other firms make airframes and composites. These structures and parts can be built in small sites with civilian cover. Subcontractors also provide electronics, optics, and assembly for large state firms.

There is also a research and reverse-engineering layer feeding future capability. IRGC-linked organizations and university-connected firms have spent years exploiting captured foreign UAVs, absorbing design features, and passing that knowledge into the wider ecosystem. That process does not end when a production building is destroyed.

The same logic works for procurement.

This is where the factory strike model is weakest. Iran’s drone industry does not survive on domestic production alone. It depends on an external procurement network that sources machine tools, electronics, navigation components, sensors, and other dual-use items through layers of intermediaries.

That network adapts quickly.

On February 25, 2026, just three days before Epic Fury began, the US Treasury sanctioned three Turkey-based companies acting as financial intermediaries for Mado. One had been incorporated in Istanbul with minimal declared capital only weeks earlier and was already processing transactions tied to sensitive machinery purchases. The pattern is familiar: shell companies appear, move money, get sanctioned, and are replaced. The underlying demand does not disappear just because one intermediary does.

The China-linked side of the network is even more mature. Treasury actions in late 2025 targeted Chinese and Hong Kong-based actors supporting Mado’s sourcing efforts, including intermediaries who arranged supplier access, travel, and procurement activities on behalf of Iranian defense entities. March 2026 designations further expanded that picture, identifying entities in Hong Kong, Taiwan, and China that were procuring technology for HESA even as its facilities were under attack.

These supply routes are not confined to one region. Treasury uncovered Ukraine-based shell firms moving items for HESA. Turkey, China, Hong Kong, Taiwan, and Ukraine show the same truth: procurement adapts, relocates, and grows.

These networks are not peripheral. They are the circulatory system of Iran’s drone program.

Engines, navigation electronics, sensors, precision tooling, and other critical inputs move through relationships like these. Striking a factory in Isfahan disrupts the flow but does not stop it.

That does not mean Iran is infinitely resilient. There is a lazy version of this argument that treats Shahed production as something that can be reassembled anywhere, by anyone, at any time. That goes too far.

There are real bottlenecks.

Engine production is the main one. Building reverse-engineered engines requires precision, stable supply chains, and expertise not available in small shops. Turbojets need even more skill. Suppressing engine output and its supply chains puts real pressure on the system.

Guidance and navigation electronics are another major limit. Shahed drones found in Ukraine use many foreign-made parts from Asia, Europe, and the US. Cutting off these supplies may hurt Iran’s capability more than bombing factories.

Most of this ecosystem is hard to suppress with airstrikes. Airframe work, composites, integration, and assembly are dispersed, lower profile, and easy to hide in dual-use sites, unlike large facilities targeted by satellites.

Three weeks of combat have stress-tested both sides of this equation. US officials have pointed to steep declines in Iranian drone attack rates since the opening phase of the war, claiming a 95 percent reduction from opening-day levels. But launch rates are not the same thing as production capacity, and neither is a clean proxy for reconstitution potential. On March 11, the day after the Pentagon briefing citing an 83 percent reduction, Iran conducted what it described as its 37th wave of attacks, striking targets across six Gulf states and hitting vessels in the Strait of Hormuz. The comparison to the 1991 Scud hunt is instructive: US forces with full air superiority and extensive intelligence support failed to achieve a single confirmed kill against Iraqi mobile launchers, a system that was larger, more infrastructure-dependent, and slower to deploy than the Shahed.

Prewar stockpile estimates varied widely, ranging from several thousand to well above 10,000 drones. That variance alone makes estimating precise degradation nearly impossible. Even discounting that figure heavily, the broader problem remains: the coalition is not dealing with a few factories at fixed coordinates. It is dealing with an industrial network.

There is now evidence that reconstitution may not be purely domestic.

Geran-2 debris bearing Russian serial markings was recovered near the port of Jebel Ali in Dubai after UAE air defenses intercepted a wave of Iranian drones in early March. Defense Express analysis of the serial number, in the 10,700 range, traced the unit to Russia’s Kupol plant in Izhevsk, with a production date corresponding to spring or summer 2024. The drone incorporated Russian modifications, including the Kometa-M jam-resistant navigation system, a feature absent from Iranian-produced Shaheds. Whether Russia supplied finished units to replenish stockpiles after Israeli strikes in 2025 or transferred them ahead of anticipated US action remains unclear, but the physical evidence confirms the cooperation is now bidirectional.

Defense intelligence reporting from early March separately indicates that Russia is considering supplying Iran with the Geran-3 and Geran-5, upgraded variants incorporating jet propulsion, an advanced guidance architecture, and battlefield modifications developed over years of large-scale use in Ukraine. The Geran-5 uses a conventional aerodynamic layout resembling a winged cruise missile rather than the triangular delta wing of the original Shahed, and is powered by a Chinese-origin turbojet engine. If those transfers materialize, Tehran would receive back its own foundational designs after extensive Russian engineering iteration, a technology loop no existing sanctions framework was designed to interrupt.

That changes the reconstitution calculus. The question is no longer just whether Iran’s domestic ecosystem can regenerate quickly enough. It now includes whether an externalized industrial reserve, built over years of wartime adaptation in another theater, can absorb the shock and restore the system’s capability.

Epic Fury has clearly degraded the visible nodes of Iran’s drone enterprise. The flagship factories and known bases that defined the public map of Iran’s drone program have been hit. That is a meaningful operational achievement.

But the harder question comes after the strike imagery.

The real issue is not whether Iran can rebuild the same facilities at the same coordinates. It is whether the wider ecosystem of private firms, subcontractors, procurement agents, and dispersed workshops can restore production capacity faster than the coalition can identify and suppress it.

The sanctions record suggests that the ecosystem has been adapting under pressure for years. It cycles through front companies, shifts procurement routes, exploits dual-use cover, and distributes work across small, low-visibility nodes that do not present the same target profile as a major factory complex.